Initial reaction

Drew O’Neil discusses fixed income market conditions and offers insight for bond investors.

Global conflicts and other major geopolitical events can lead to a wide range of consequences across financial markets. Predicting the outcome of these events and the corresponding effects on the markets can be difficult at best. In this commentary, I’m not going to try to predict any outcomes or long-term effects but rather want to cover how markets have reacted so far and highlight some opportunities that have been created.

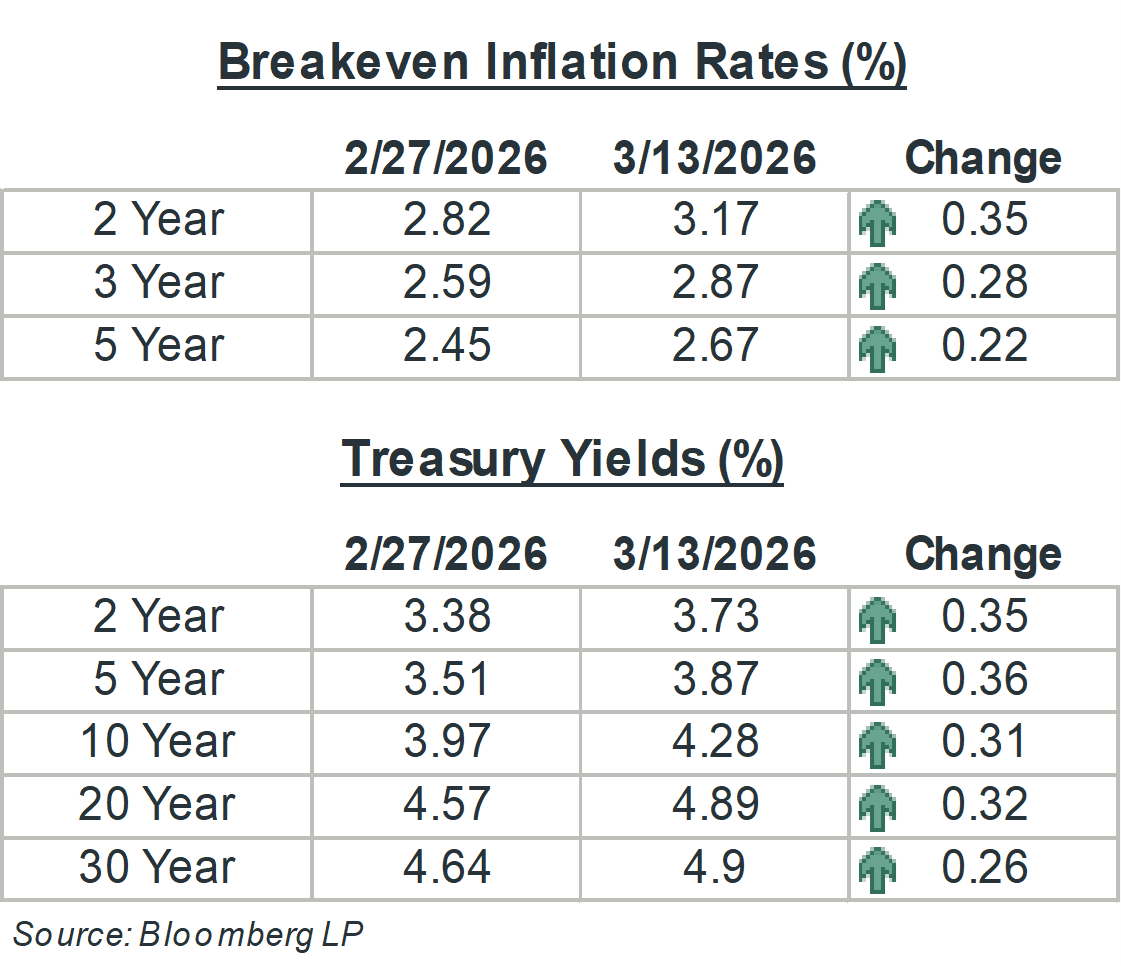

The traditional reaction to a major military conflict is a flight to quality, also known as a “risk-off” trade. In the fixed income arena, this typically leads to Treasuries rallying (prices higher, yields lower). What has ensued over the past few weeks is exactly the opposite. Why? Markets appear to be more concerned with the potential impact that the Iran conflict could have on inflation than the need to seek out the safety of Treasuries. The price of oil has risen from the mid-$60’s just prior to the conflict to the mid-$90’s just two weeks later, an increase of over 40% (price per barrel of West Texas Intermediate). The longer that these elevated price levels persist, the greater and longer an impact there is likely to be on inflation. In addition to the impacts on inflation, the cost of the war is creating further concerns among those that were already worried about the United States’ budget deficit. In a briefing to Congress last week, the Pentagon estimated that the first six days of the war cost at least $11.3 billion. Given that the estimate is likely low and we are now over two weeks into a conflict that has no clear end in sight, the concern that the war is going to lead to increased borrowing by the Federal government is a legitimate one.

As of now, the tug-of-war between a flight to quality and inflation/deficit concerns is being won by the latter. The chart on the right shows how much the breakeven inflation rates over the next 2, 3 and 5 years have changed since the start of the war. The breakeven rates tell us how much inflation the market is pricing in over each timeframe. The uptick over the past two weeks is a big part of what has raised Treasury yields, as increased inflation expectations tend to push yields higher. As shown in the chart, Treasury yields are up by ~25 to 35 basis points over the same timeframe.

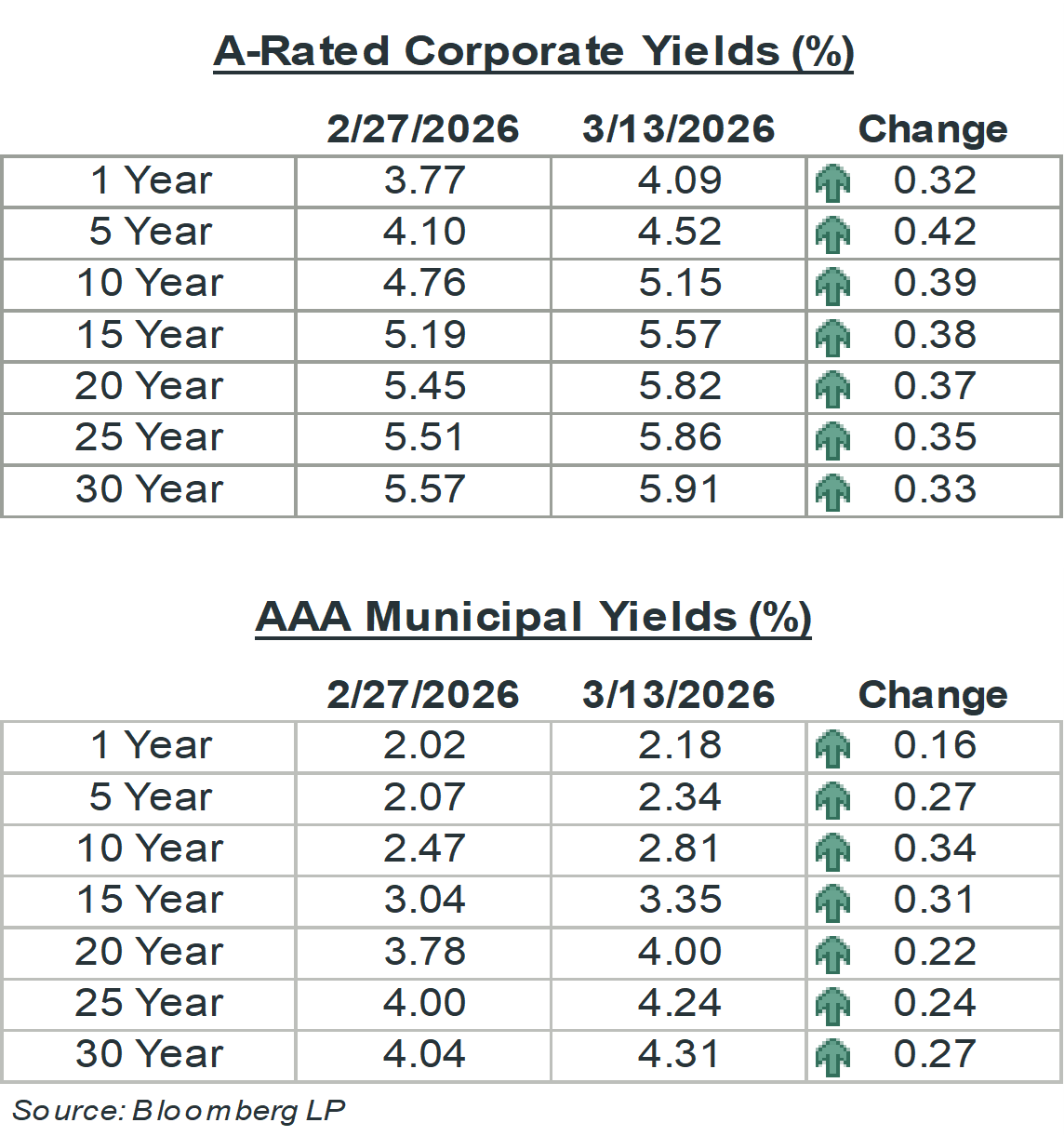

What’s the takeaway for fixed income investors? High-quality yields across the fixed income landscape have become more attractive, creating a good opportunity to lock in attractive yields. In the intermediate and long-end of the municipal curve, which is where most of the value is in that market, yields are 25 to 35 basis points higher. This translates to taxable equivalent yields of 7% or higher for top tax bracket investors. In the corporate market, in addition to higher benchmark (Treasury) yields, spreads have widened over the past few weeks, helping to push yields even higher. A-rated yields in the intermediate part of the curve are higher by 30 to 40 basis points, reaching levels not seen since last July. As the past few weeks have reminded us, there is a lot of uncertainty in the world and things can change quickly. What we do know is what is available right now: high-quality bonds offering attractive yields that can be locked in for years to come. Contact your financial advisor to see available fixed income opportunities that line up with your long-term financial plan.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

To learn more about the risks and rewards of investing in fixed income, access the Financial Industry Regulatory Authority’s website at finra.org/investors/learn-to-invest/types-investments/bonds and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) at emma.msrb.org.